Cash Flow

Cash Flow Management at the $1M–$30M Stage

Revenue growth and cash tightening often happen at the same time. That is not a coincidence.

John Regan, CPA | 10 min read

Why Cash Gets Harder to Manage as Revenue Grows

I've seen this dozens of times. A founder hits $10M and has less cash visibility than they did at $1M. Not intuitive — but it happens every time. Customer terms stretch, inventory builds, payroll doubles, and the gap between when money is earned and when it lands in the bank widens faster than most founders expect.

A company can grow revenue 40% year over year and run out of cash at the same time. The income statement won't show you that. The cash flow statement will. Most founders at this stage aren't reading it closely enough — if at all. That's where the real risk lives.

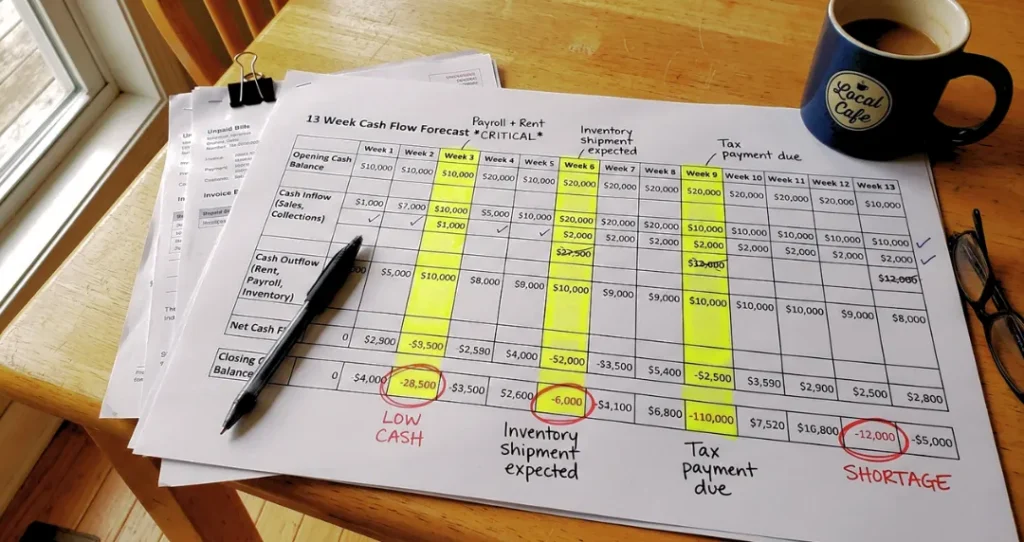

The 13-Week Cash Flow Forecast

I build one for almost every client we bring on. It's the first thing I ask for — and almost always the first thing that's missing.

This isn't a revenue estimate or a budget. It's a rolling, week-by-week model of every dollar in and out over the next 90 days — built from real receivables, real payables, real payment timing. With it running, you can see a cash crunch 3–6 weeks before it arrives. Without it, you find out the week it becomes a crisis. By then, your options are bad.

What goes into a real 13-week model

- Aged receivables mapped to expected collection weeks — actual patterns by customer, not just due dates

- Committed payables: vendor terms, payroll cycles, rent, debt service

- Planned capex and discretionary spending that can flex

- Credit facility availability and draw triggers

- Weekly ending cash balance with a defined floor

I worked with a CPG brand at $14M revenue — growing 35% year over year, strong retail presence, good margins. The CEO was focused on a Q4 retail expansion that required a significant inventory build starting in August.

We came in during the summer. The first thing I did was build the 13-week forecast. Within a week, we could see that the inventory purchases, combined with slow Q3 collections from their largest distributor, were going to leave them with less than three weeks of operating cash by mid-October.

In August, that's solvable. We had time to call the distributor, tighten the collection schedule, and line up a short-term credit facility before anyone was under pressure. The terms we got were reasonable. The process was orderly.

Without that model? They would have discovered the problem in late September. And I've seen what that looks like — emergency calls to lenders, unfavorable terms, founders negotiating from desperation instead of from a plan. The 13-week forecast didn't save the company. But it saved the CEO three months of stress and probably 200 basis points on the cost of capital.

Receivables: The Most Controllable Lever You're Ignoring

You've already done the work. The cash is sitting in unpaid invoices. DSO — Days Sales Outstanding — is the number I look at first. For most B2B businesses, above 60 days is a problem. Above 75, it's a significant one.

Cutting DSO by 10 days on $10M in revenue frees up approximately $275K in cash. No new customers, no price increases. Just getting paid faster on revenue you've already earned. The levers aren't complicated — they're just not being pulled.

- Invoice immediately. The day the work ships or the service is delivered — not at month-end.

- Set terms and enforce them. Net-30 means nothing if you don’t follow up on day 31.

- Know your chronic slow payers. That information changes your commercial decisions.

- Offer early payment incentives where it makes sense. 1% net-10 is cheap capital versus a credit line.

- Reprice slow customers at renewal. They’re imposing a working capital cost on you. Reflect it.

"If you ask me what the single most common cash flow mistake I see at this stage, it's this: the founder thinks they have a revenue problem when they actually have a collections problem. The money's already been earned. Go get it."

Inventory and the Working Capital Wedge

If you make or sell physical products, inventory is your biggest cash consumer. In a typical product company, you buy inventory 12 weeks before it sells — and your customer pays 60 days after it sells. That's 5–6 months of cash tied up in a single cycle. At scale, that wedge becomes a real constraint on growth.If you make or sell physical products, inventory is your biggest cash consumer. In a typical product company, you buy inventory 12 weeks before it sells — and your customer pays 60 days after it sells. That's 5–6 months of cash tied up in a single cycle. At scale, that wedge becomes a real constraint on growth.

The CFO needs to be in the inventory conversation before the PO goes out — not when we're reconciling the balance sheet. Inventory decisions are cash decisions.

What we model for product-company clients

- Days Inventory Outstanding (DIO) by SKU or product category

- Cash conversion cycle: DIO + DSO minus Days Payable Outstanding

- Inventory build requirements tied to revenue projections and seasonal demand

- Supplier term optimization — every day you extend payables is a day of free financing

- Reorder triggers modeled against cash availability, not just stockout risk

Debt vs. Equity for Working Capital

When founders hit a working capital crunch, the default is to raise equity. For working capital, that's almost always the wrong tool. Working capital is a timing gap — money tied up in receivables or inventory that comes back. Timing gaps should be funded with debt.

Equity is for permanent capital: new markets, headcount, product lines. Using it to bridge a receivables collection cycle is like using a mortgage to cover a month of expenses. The right debt options at this stage:

- Revolving credit facility: Draw when you need it, repay when receivables collect. Cleanest solution for most $5M–$30M companies.

- Asset-based lending (ABL): Secured against receivables or inventory. Borrowing base grows as your business performs.

- Inventory financing: Purpose-built for product companies with significant inventory cycles.

- SBA 7(a) loans: For earlier-stage companies that don’t yet qualify for conventional revolvers.

The catch: lenders want clean GAAP financials and the ability to report on covenants. Fix your finance function first — then the debt is available when you need it.

Cash Visibility Is a Leadership Habit

I've worked with companies that have good controllers and decent bookkeeping but terrible cash visibility. The data exists. No one's looking at it. Every founder who's hit a serious cash problem tells me the same thing: "We knew things were getting tight, but we thought it would work itself out." That's not a finance failure. That's a leadership failure.

Cash visibility has to be a CEO-level habit. Here's what that looks like:

- Weekly cash review. 15 minutes with a good model. Current balance, expected inflows for the next four weeks, committed outflows.

- A defined cash floor. The number below which you will not go without taking action. Written down. Agreed on. Tracked.

- Clear escalation triggers. If week-eight projected cash drops below the floor, who gets notified and what happens? Build the protocol before you need it.

- Cash in every board package. If your board isn’t asking for a 13-week outlook, start providing it anyway.